Bare Trust Deed

Our Bare Trust Deed template:

- Now over 400 simple bare trust deeds sold!

- A trust deed commonly used to pass assets to a child

- Also used for a corporate trustee to hold a cash investment

- Drafted by an expert UK solicitor

- Legalo’s money-back guarantee

- Full guidance notes and customer telephone support included

How Does It Work?

-

1. Download

-

2. Edit

-

3. Print

-

4. Sign

MD, Legalo Ltd; Solicitor; Notary Public

{kind=link}

This is our template for a Bare Trust Deed. This template precedent allows you to create a new trust and sets some basic rules and powers for the trustees.

How to Use our Deed of Bare Trust

You can download our template document in Word format. Once you have downloaded it, you can easily customise the template deed to meet the specific requirements for the trust that you are setting up.

A UK solicitor practising in England has carefully prepared our precedent template. We include detailed guidance notes that take you through every step in completing the bare trust deed template.

If you have any questions when completing the deed, you can speak to a solicitor. Just use our free customer support telephone line. The same applies if you have any questions before you buy the document. Please do call us; we are on hand to assist you.

Over 400 happy clients have bought our Bare Trust Deed

What is a Bare Trust Deed?

A bare trust deed is also commonly known as a ‘simple trust’. This is because of the simplicity in setting it up, and in its operation.

Setting up a bare trust creates a legal arrangement where a trustee holds certain assets for the benefit of a beneficiary.

The beneficial interest in the asset(s) is transferred by the trust deed to the beneficiary but the legal interest is transferred to the Trustees of the trust who hold the asset for the benefit of the beneficiary.

With a bare trust the beneficiary has the right to both the income derived from the asset held in trust, and to the asset itself. Accordingly, the role of the Trustee is purely administrative and they must manage the asset held in the trust for the benefit of the beneficiary.

As we mention above, people often use a bare trust deed to arrange for a trustee to hold assets for the benefit of a child. People also commonly use them as part of tax-planning strategies, where an asset can be gifted via the trust and become a Potentially Exempt Transfer. Read our guide to the 7 year rule for more information on this.

It is the simplicity of the bare trust deed that makes it a popular choice for people who want to transfer the beneficial interest in an asset, whilst maintaining control of the asset via the trust.

Legal framework for Simple and Bare Trust Deeds

In the UK, specifically in England, the creation of a simple or bare trust is governed by common law principles and legislation.

Common law principles, i.e. those developed by the courts, set out the set out the legal requirements for a valid trust document. Legislation governs how the trustees of the trust must operate a simple trust.

The Trustee Act of 2000 and the Trusts of Land and Appointment of Trustees Act 1996 are the most relevant of the legislative documents.

Legal Requirements for a Bare Trust

There are several legal compliance and document requirements that are relevant to a bare trust deed that you should be aware of.

Compliance Requirements

The Trustees of a simple or bare trust are required to adhere to the following legal requirements:

- Acting in Good Faith: The Trustees must at all times act in the best interest of the beneficiaries.

- Maintaining Accurate Records: the Trustees must at all times keep accurate records of the trust’s assets and all of the transactions related to those assets.

- Tax Reporting: The trustees are obliged to make sure that where required all necessary tax filings are completed for the trust. With a bare trust any income will be taxed as if received directly by the beneficiary and so under present legislation it will not be necessary for the trustees to complete any tax filings, other than registering the trust.

Document Requirements

There are several requirements that must be met for a bare trust deed to be legally valid. These are:

- Trust Declaration: the trust deed must identify the trust, the trustee, and the beneficiary, and confirm the assets being held in the trust.

- Trustee Powers: The administrative powers of the trustee, such as the power to manage or invest the trust assets must be detailed in the document.

- Beneficiary Rights: The trust deed must clearly state the beneficiary’s absolute right to the trust’s assets and income.

- Governing Law: The deed must confirm that the trust is governed by the laws of England and Wales (or Scotland).

When to Use a Bare trust Deed in the UK

There are several common situations where a bare trust is used. These include:

- When you are passing assets to a child (a trust is essential if the assets are, or include, land and buildings in England and Wales, or UK shares);

- Spouses owning investment property and, later, changing their ownership percentages;

- Personal injuries trust;

- Criminal injuries compensation trust;

- A Disabled Person’s Trust (where it is impractical to use a discretionary trust with two or more beneficiaries); and

- Having a corporate trustee receive a cash sum for investment.

Please note that in relation to a Disabled Person’s Trust, if this is set up as a bare trust, then the value of the trust assets might be taken into account when means-testing the disabled person’s Benefits applications.

The most common of the situations is where a bare trust is used is where money is to be left to a child or grandchild. Read our guide to ‘The Best Ways to Leave Money to Grandchildren’ for more information on this, if it is relevant.

It is common for a bare trust deed to specify that the asset passes to the child once they reach age 18.

Note that once the beneficiary turns 18 years of age (16 in Scotland), then the trustee must act on their instructions.

As a “bare trust”, there is nothing to stop the beneficiary asking for the property or assets (and any income that arises from the assets) in the trust to be transferred immediately to the beneficiary. This is providing the beneficiary is at least 18 years old in England or 16 in Scotland.

What about a Discretionary Trust?

If you are considering putting an asset into a bare trust for the benefit of a person that is over 18 years of age, you may want to consider a ‘Discretionary Trust’. This also applies if you want the assets to remain in the trust for at least a few years after the beneficiary turns 18.

We won’t be offering a discretionary trust deed template at Legalo. This is because they (a) are much more complex, and (b) have complex tax arrangements, as they are designed to save tax. The bare trust deed is a much simpler document.

Bare Trust v Discretionary Trust

If you are unsure whether a bare trust is preferable in your circumstances, we review the key features and the differences between a Bare Trust and a Discretionary trust below.

Bare Trust (also known as a ‘Simple Trust’)

- Beneficiary Rights: The beneficiary once 18 years of age has an immediate and absolute right to the trust’s assets and income. The beneficiary can demand the transfer of the asset(s) covered by the trust at any time, provided they are of legal age and have full mental capacity.

- Trustee Role: The trustee’s role with a Bare Trust is largely administrative. Essentially they hold the asset(s) on behalf of the beneficiary and act according to the requirements of the Trust Deed, or once the beneficiary turns 18 the directions of the beneficiary.

- Flexibility: A Bare Trust is very simple to set up using a bare trust deed. However, with a bare trust there is no flexibility for changing the beneficiary, or the allocation of assets between beneficiaries once established. This can often be seen as both an advantage and disadvantage depending on your requirements. Grandparents often prefer the peace of mind in knowing the grandchild will receive the asset.

- Taxation: The income from the trust is generally taxed as if it was generated directly by the beneficiary. This means that the income is taxed at the beneficiary’s rate of tax. In the case of a child the parent will pay the income tax, if any, where it is over £100.

- Common Uses: A bare trust is most often used for holding assets for minors until they reach 18 years of age and where beneficiaries are clear and unchanging.

Discretionary Trust

- Beneficiary Rights: With a discretionary trust the beneficiary does not have an absolute right to the trust’s assets covered by the trust. Instead, the terms of the trust give the trustee discretion over how and when assets and income are distributed among the beneficiaries.

- Trustee Role: Unlike a bare trust, the trustee has a lot of control over the asset and the ability to decide how the named beneficiaries are to benefit from the asset in the trust. The trust deed will provide guidance to the trustee to assist them in making their decisions.

- Flexibility: Discretionary trusts are by their nature very flexible. The trust deed gives the trustee the power to decide how to apply the income and assets held in the trust. This can enable the trustee to allocate income or assets based on the changing circumstances of the class of beneficiaries listed in the trust deed.

- Taxation: The trust itself is often subject to its own tax rates, which can be higher than personal tax rates. However, trustees may have options to distribute income in a tax-efficient manner.

- Common Uses: People generally use this type of trust for managing more complex family situations where they want flexibility.

Summarising the differences

In brief, a bare trust is a simple trust arrangement where the settlor defines the the beneficiary and then cannot change the beneficiary. Once they are 18 years of age (or 16 in Scotland), they have an absolute right to have the trust asset transferred to them, if they wish.

Conversely, discretionary trusts provide for flexibility and give the trustees control over how they distribute the income and assets in the trust.

You can read more on the types of trust on the Government website.

If a discretionary trust better suits your circumstances, firstly, make sure you have selected at least 2 beneficiaries, as this is a fundamental requirement for a discretionary trust.

You can’t have a discretion over who gets what if there is only 1 possible beneficiary in the trust. If this is OK, then find a solicitor to help you set up the discretionary trust and ensure it is tax compliant.

When to use a Bare Trust Deed

If a bare trust is the right type of trust arrangement for your situation then you can use our bare trust deed for the holding of any type of property, for example:

- Cash;

- Shares;

- The proceeds of a personal injury claim or a criminal injuries compensation claim; and / or

- Land and / or buildings.

When you complete the template trust deed, simply set out in the schedule to the deed what assets are to be in the bare trust.

Bare Trust Deed v Deed of Gift

If instead of setting up any form of trust, you are happy to make an outright gift now, you can instead use our template for a Deed of Gift. With this type of deed, you create an immediate transfer of the asset to the beneficiary.

The deed provides evidence of the gift and the particular date that the settlor made it. This is important as evidence to address potential inheritance tax issues.

You cannot use a deed of gift if the gift is to a person under the age of 18 in the UK, where the gift is of:

- land and buildings in the UK or

- UK shares.

This is because in the UK minors cannot legally own land and shares. In this situation, it would be necessary to use a bare trust deed to transfer the beneficial interest in the asset. The minor can then take legal ownership of the asset once they reach 18 years of age.

When not to use a Bare Trust Deed

Firstly, do not put assets into a bare trust, or any type of trust, if you are insolvent or bankrupt. A trustee in bankruptcy can unravel such a move, as an attempt to defraud your creditors.

Secondly, do not put assets into a trust to reduce your net worth when you are on Benefits or applying for Benefits. This is illegal and constitutes benefits fraud. This also applies, as noted above, in relation to a Disabled Person’s Trust: a bare trust usually won’t help you here.

Thirdly, you should not put an asset, such as property, into a trust for someone, but aim to receive the income arising from it, such as rent or dividends. Once you have set up a trust, all the income would belong to the trust as of the date you put the asset into the trust.

Bare Trusts for Children

The most common use of our bare trust deed template is for when you are passing assets to a child. Most notably this involves grandparents wishing to pass assets to their grandchildren. This usually involves money, property or shares.

The assets will remain in the trust, and managed by the trustees, until the grandchild reaches the necessary age. However, note that if you set the age at over 18 years of age, the child once becoming an adult can require that the trustee transfers the asset to them.

A trust would be necessary in the case of passing land in England and Wales to a child. This is because the law does not permit children to be on the legal title (the title deeds) to the land until they reach adulthood at age 18.

In the meantime, they could be the beneficiary of the land under a bare trust until they become 18 years old. At that point, they could have the title to the land transferred to them.

Personal injury trusts

You can use our bare trust deed to create a personal injury trust (or a criminal injuries compensation trust, which is essentially the same thing). You would need at least 2 trustees in each case, but the beneficiary could be one of those trustees.

This means the injury compensation is paid into the trust and the trust is held for the benefit of the beneficiary, but importantly the money in the trust fund is not counted as being capital owned by the beneficiary for the purposes of their entitlements to Benefits. So your Benefits should not be adversely affected if you set up a trust to hold the compensation in this way.

This is a lawful arrangement and is not counted as “benefits fraud”.

Use of a Trust for Spouses Changing Ownership Percentages

Sometimes, when a couple has an existing investment property, the husband or wife will choose to gift part of the property to the other spouse.

It might be for tax reasons. (Such a gift between spouses is free of tax.) Firstly, if they own it as joint tenants, they will use a Notice of Severance to alter this to being owned by them on a tenants-in-common basis.

They would file an SEV form with the Land Registry to note this change. Then they can hold the property in unequal percentages of their choice.

For this, they can either (a) file a TR1 with the Land Registry, or (b) they can use our Bare Trust Deed, to have both spouses declare the new ownership basis.

The trust deed avoids the need for filing a TR1 to change the ownership percentages on the title. It also keeps your ownership percentages off the public register.

FAQs on Simple Bare Trusts

People often have questions about bare trusts and their use. We address a few of the most popular ones below.

Is a Simple Trust the same as a Bare trust?

Yes, a simple trust is exactly the same as a bare trust. The two terms are used interchangeably both to describe the same trust structure which the bare trust or simple deed template covers.

Is a bare trust a good idea?

If you want to set up a trust, a good, simple solution is a bare trust. It is much easier to set up than a discretionary trust, as it is not trying to gain a tax advantage, so has few requirements to comply with.

It is a very good solution when you are holding the assets in trust for a child. If you want to give shares to a child, then setting up a trust to do this is the only option, as UK laws do not allow children to buy shares in the UK.

Do you need a trust deed for a bare trust?

Yes. The document you use to set up the trust is the trust deed. The person creating the trust. must sign it. The deed must name at least one trustee and one beneficiary, and list the assets that the settlor is putting into the trust. Lastly, when the person gifting the assets to the trust signs it, an independent adult must witness their signing it.

What documents are needed for a bare trust?

A trust deed is the only document you need to set up a trust. The trust deed will specify who the initial trustees are.

You can also set up a bare trust through your Will. In that case, the Will is the only document you need. Legalo’s Will templates are simple and do not include any trusts, except for the Will with a life interest trust.

Does a bare trust have to be in writing?

Yes in practice. Otherwise, you’d have no evidence that you had created a trust (or the date you did so, the amount of assets that you put in the trust, or who the trustees are who the beneficiaries are) if it were not in writing.

In short, you’d be in a total muddle. HMRC would have a problem with that. To put land into a trust, there is an absolute legal requirement that you do so in writing.

What are the legal requirements of a bare trust?

There must be a deed in writing, signed by the person(s) setting up the trust (the settlor(s)), specifying as a minimum:

- the date you or they created the trust;

- what assets you or they put into the trust;

- who the trustees are;

- who the beneficiaries are; and

- if there is more than 1 beneficiary, in what proportions they each own the assets.

How much does it cost to set up a bare trust in the UK?

While it will several hundred pounds to have a solicitor set up a simple bare trust for you, you can save a lot of money by using a trust template from Legalo.

Our template is just £54.95. It comes with a full written guide, to make filling it in easy and fast.

How do you draft a bare trust?

While you can do so yourself, Legalo’s bare trust deed template (and its written guide) make this very easy for you to do. It also ensures you cover all the necessary aspects.

Can I draft my own bare trust deed?

You can do so, and you will find that a template from Legalo makes it so much easier to do this, and it helps you avoid mistakes or leave anything essential out. You don’t have to use an expensive solicitor when you can do this for yourself with the help of a Legalo template.

Does a bare trust deed have to be registered with HMRC?

Yes. Due to a recent change in the law, you need to register all trusts with HMRC shortly after creation. This does not necessarily mean that you have to pay tax as a trust. See the Government website for registration details here.

A bare trust saves no tax, so also incurs no tax for which it is liable. The people liable for the tax are either:

- the beneficiaries ; or

- their parents, in the case of a trust set up by parents for their children.

See the next question about taxing a bare trust.

Does a bare trust need to complete a tax return?

A bare trust is “transparent” for tax. So this means it does not file its own tax returns or have its own tax allowances. Instead, generally the beneficiaries are the ones liable for any tax. For example: tax on income (if any) that the trust generates for the assets in it.

For example, this would include interest on a bank account or rent on an investment property. There is an exception where parents have put assets into trust for their children. The parents remain liable for the tax in this case.

How many beneficiaries can a bare trust have?

There is no limit on the number of beneficiaries a bare trust can have.

If more than 4 people together own a piece of land in the UK, then (as you can only put a maximum of 4 on the title deeds at the Land Registry) you would need a declaration of trust or bare trust deed, to cater for the other owners.

Who controls a bare trust?

Until the beneficiaries intervene, the trustees control the trust and run it from day-to-day. However, the beneficiaries can ask for you to transfer the property directly into their names. This is because it is a bare trust.

So ultimately they control it, as they can bring it to an end. There is an exception to this when the beneficiary is under 18, or in Scotland under 16.

A child cannot ask for you to transfer the assets to them until they reach such an age. So, until then, the trustees genuinely control the assets in the trust. A transfer of all of the assets to the beneficiaries will terminate the trust.

Nominee Trusts

You can also use our bare trust deed to set up a “nominee trust”. This is very similar to a bare trust.

Aside from our general bare trust deed, we also have nominee trust deeds for the following more specific purposes:

- Declaration of Trust for shares;

- Declaration of Trust for domain names; and

- a Declaration of Trust for a bank account.

For more about bare trusts from Wikipedia, click here. For more about nominee trusts from Wikipedia, click here.

Register Your Bare Trust with HMRC

As of 6 October 2020, you now need to register all new trusts with HMRC. This applies even to ones that are not taxable. You have 90 days from the date of creation of the trust to register it. Find out more and register here. Don’t forget to register your bare trust.

This is fairly straightforward to do by yourself, so you do not need a professional to help you. However, you will need a lot of information. So read HMRC’s notes and gather what you need, before launching into it.

Guide to the Clauses in our Bare Trust Deed

Below, we have set out the key points from the written guide to the Bare Trust Deed template.

If you have any questions on our bare trust deed, please contact our customer support telephone line.

Numbered clauses

1. Interpretation

Normally, this clause defines the main terms used in the deed.

If the Beneficiary is to be a party to the trust deed (about which see clause 6 below), then, delete the definition of “the Beneficiary” in this clause. If they are not to a party to the deed, then fill in the Beneficiary’s details here.

For the definition of “Trust”, you can fill in a name for the trust, which can be useful when opening a bank account or registering it with HMRC. A typical format for naming a trust has been suggested, but you can name it what you like.

For the definition of “Trust Fund”, choose which option you want and complete the details. This is suggested as either:

- a set amount put into the trust in cash by the beneficiary (for example, when money is being held to be invested by a corporate trustee) or the settlor; or

- assets listed in a schedule.

In the Trust Fund definition, you can set the name of the person setting up the trust as that of:

- the beneficiary; or

- the settlor (i.e. the person creating the trust, if not the beneficiary) if it is someone else.

You have the option to list and specify the assets in the Schedule if it is not simply cash. If you don’t use the Schedule option, please delete the Schedule (near the end of the deed).

For the definition of Trust Period, you can:

- leave this without a limit (as written); or

- put a set period if you prefer.

Select where the assets in the trust came from: the Beneficiary, the Trustee or the settlor.

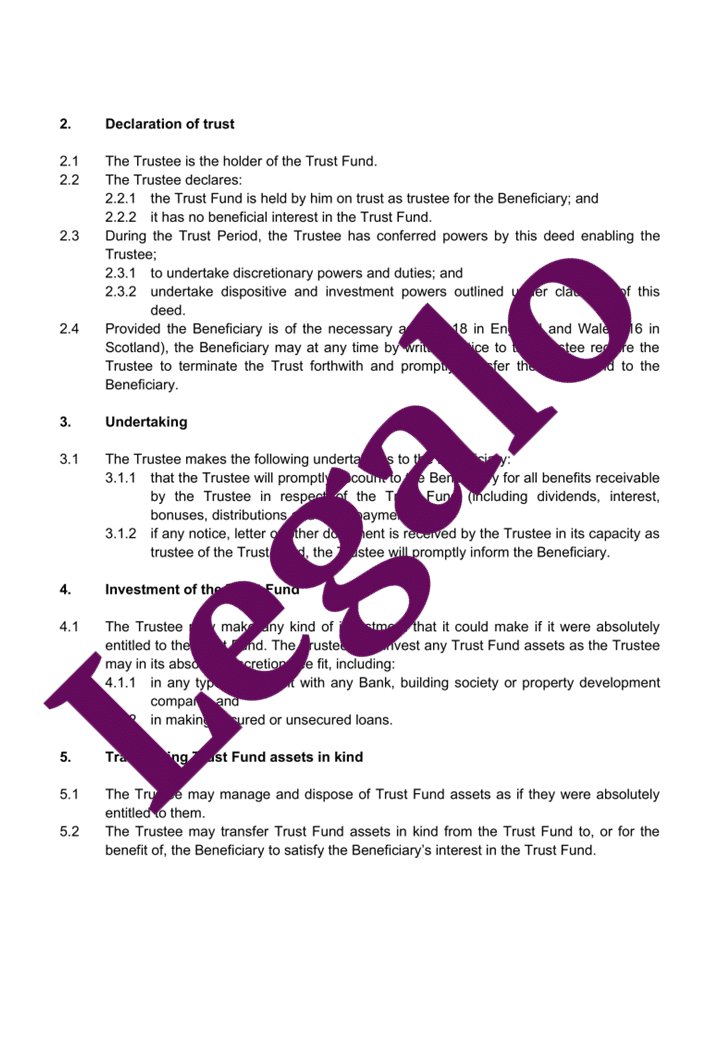

2. Declaration of trust

This is the main clause which states that the trust fund is held in trust. It also sets out some basic powers the trustee has to manage the trust fund. Clause 2.4 confirms that the beneficiary (if an adult) can ask the trustees to transfer the assets to them.

3. Undertaking

This clause sets out some of the trustee’s duties.

4. Investment of the trust fund

This clause adds to the powers of the trustee to invest the trust fund. If the trust fund is not an active investment fund (e.g. if it is land or buildings), then you might want to delete the whole of this clause.

5. Transferring Trust Fund assets in kind

This clause states that:

- the trustee is not necessarily obliged to sell assets (e.g. investments) in the trust fund,

- but could transfer them back to the beneficiary as they are.

6. Indemnities

The purpose of this optional clause is to give some comfort to a corporate trustee. It is about their not being liable for the consequences of following investment choices that the beneficiary makes. If this does not apply, you can delete the whole of this clause.

If you are deleting this clause, then the beneficiary does not need to be a party to the trust deed. In such case:

- delete the party clause for the beneficiary at the start of the deed;

- delete clause 6; and

- delete the signature clause for the beneficiary at the end of the deed.

The Schedule, the assets

As mentioned above, if the assets held in the trust initially are just cash, you can omit listing them here. Otherwise, list here the principal assets, such as freehold or long leasehold property, bank accounts, shares and other investments. We suggest you list their present values too, but this is entirely optional. If there are a lot of shares in various companies, you could:

- describe them in general terms, rather than listing them individually; or

- refer to a separate list where they are all detailed.

The guide also tells you how to sign the deed correctly.