Loan Agreement

Our Loan Agreement template:

- Suitable for unsecured loans

- Full guidance notes included

- Plain English; easy to edit and complete

- UK-solicitor-drafted template for reliability

How Does It Work?

-

1. Download

-

2. Edit

-

3. Print

-

4. Sign

MD, Legalo Ltd; Solicitor; Notary Public

{kind=link}

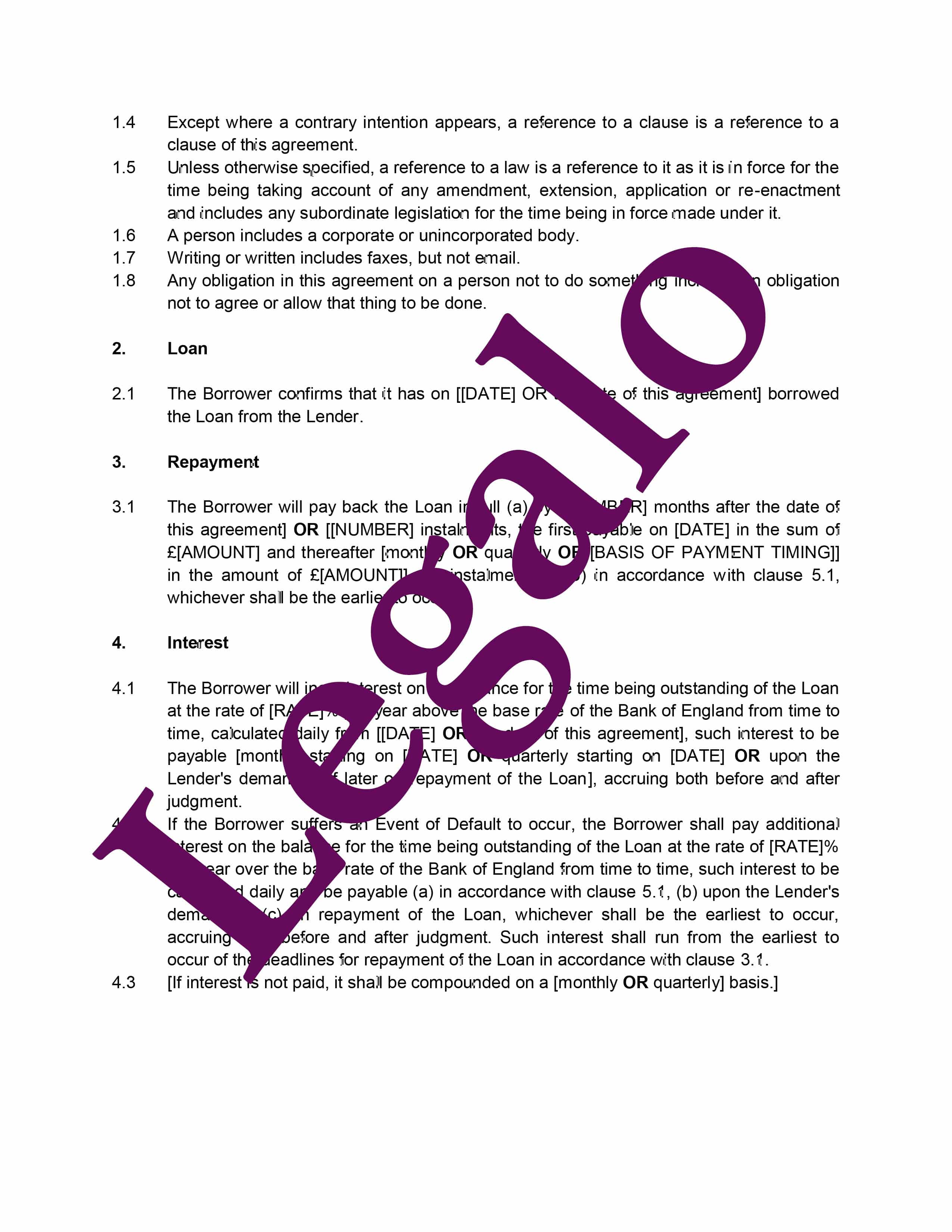

Use our template loan agreement to document a private loan. In order to avoid arguments at a later stage, it is always advisable to document in writing:

- the giving of the loan, and

- the terms of its repayment (including interest).

About our Loan Agreement Template

We have written this loan agreement template in plain English. It is simple, yet comprehensive enough to document the terms of the loan clearly. This template is for an unsecured loan.

You would commonly use this type of private, or personal, loan agreement to document a loan made between:

- family members or close friends, or

- loans to, or between, companies.

The latter would include a director’s loan to his company.

Do you need a Secured Loan Agreement instead?

Loans to strangers (or limited companies) should ideally be (a) guaranteed or (b) secured against a valuable asset – if this applies, try instead our:

For director’s loans, you should also consider if you want to take security at the point you make the new loan to the company, because adding security at a later stage (particularly when the company may be struggling financially) may well be invalid. The agreement template is in Word format and is governed by UK law. For an overview of the agreement, see the preview of our guidance notes on the template or, for a sample, you can click the preview button to the right.

Our other loan and security templates are:

- Employee Loan Agreement;

- Family Loan Agreement;

- Loan Agreement With Guarantor;

- Secured Loan Agreement;

- Discount Package: Secured Loan Agreement with Legal Charge;

- Discount Package: Secured Loan Agreement with Debenture;

- Legal Charge; and

- Debenture.

When to use our Loan template

You should put in place a written agreement to document the terms of any modest to significant loan. With an agreement in place, there can be no subsequent dispute or arguments over the terms of the loan. It also avoids arguments that the loan was never made. It should be put in place when the loan in being made ideally; preferably not later on.

We have kept this standard UK loan template simple. You should be able to complete it within 15 minutes. Our full guidance notes that come with the template will make it easy for you to adapt this template to suit the loan you are making. If you should need any further assistance in completing your template or have any queries, then do not hesitate to contact us by telephone or email.

Our experienced UK solicitor and co-founder of this website, David, drafted this template specifically for ease of use.

If you are lending to a close family member who you trust and you don’t want security for the loan, then try our Family Loan Agreement. If the loan is to an employee, then use our Employee Loan Agreement instead.

For a list of our other loan templates, click here or use the links on the right. For Wikipedia’s commentary on such agreements, click here.

FAQs on a Loan Agreement

Below, we have answered the top questions from the Internet on loan agreements.

How do I write a legal loan agreement in the UK? How do I write a loan agreement between two parties?

To write a legal loan agreement, it is important to include details of the parties involved, specify the loan amount and interest rate (if applicable), outline the repayment terms, schedule, and any collateral security, as well as specify any late payment penalties and terms for if there should be a default. The agreement’s duration should also be specified, and both parties must sign the contract. If you want security for the loan, use our Secured Loan Agreement and Legal Charge templates.

How do I write a basic loan agreement? How do I set up a personal loan agreement?

As noted above there are various elements to include in any loan agreement. With our great template, all of the necessary legal issues are included already, so you only need to fill in your personal details and a few specifics about your loan agreement. You can then be sure that your contract will be legally valid and doesn’t miss out any of the important details.

What makes a valid loan agreement?

To ensure that your loan agreement is legally binding, you must clearly identify the lender and borrower, loan amount, interest amount, if any, and repayment schedule. Both parties’ signatures need to be included along with the date, and to add an extra layer of validity, the signing should be witnessed.

If you are operating as a business and giving credit or loans to consumers, then you need a consumer credit licence and need to comply with terms regarding making the total cost of the credit clear and specifying effective APR rates. If you don’t, you may not be able to enforce the loan agreement, so you risk effectively invalidating it.

Does a loan agreement need to be witnessed in the UK?

A witness is not required by law for a loan agreement, as it is usually signed as a simple contract and not signed as a deed.

Can anyone write a legal agreement?

Anyone can write a legal agreement such as a loan agreement, but it can often become expensive when involving solicitors. With our great template, you can write up a legally-enforceable loan agreement, while avoiding:

- the cost that hiring a solicitor would incur,

- the risk of getting the drafting wrong,

- leaving something important out, or

- the time wasted doing your own research on what should go into the draft.

Using a reputable template, like ours, ensures legal validity, that nothing critical is left out, and almost all you need to do is fill in the blanks.

What is the contract for loaning money to a friend?

A contract for loaning money to a friend would fall under a ‘Personal Loan’ document outlining the terms of a financial arrangement between two individuals. It specifies the loan amount, repayment terms, interest (if any), and any conditions related to late payments or default. It serves to protect both parties’ interests by formalising the loan, and ensuring mutual understanding and a legally binding contract. This loan agreement template is a great one to use for this purpose if you don’t require security.

How much does a loan agreement cost?

For a simple loan agreement, a solicitor is still going to charge you several hundred pounds to write an agreement for you. To significantly reduce the cost, while maintaining legal reliability, we recommend you purchase our template for just £29.95. Then you can fill in the details of your agreement yourself in your own time.

Can a loan agreement with a family member be legally binding?

Family loans can, of course, be legally binding. It is key in these cases for your family loan agreement to meet a set of criteria to make it a legally-enforceable contract, rather than one based solely on trust or on a verbal arrangement. It is often useful to have a written loan agreement in order to show the loan was intended to be repayable and was not made as a gift. Also the written agreement serves to prove the loan was made and the amount of it, in case:

- another family member queries it, or

- the borrower dies and their estate needs to repay the money.

Have a look at our checklist below for checking the validity of any loan, including a loan to a family member.

Checklist for a loan:

Make sure to be clear about the following:

- Offer and acceptance. The offer of the loan and its terms must be clearly stated and agreed upon by both parties, thus demonstrating a mutual agreement.

- Consideration. Both parties must provide something of value as part of the agreement. This is fairly clear in a loan situation.

- Intention to create legal relations. The contract must make it clear that the intent for both parties is for the agreement to have legal consequences.

- Capacity. Both parties must be willing and able to enter into a contract. They must be of sound mind, not under duress, and at least 18 years of age.

- Clarity. The terms of the agreement must be clear and easy to understand, to ensure that all parties know what they are entering into.

- Legality. The agreement must, in itself, be legal. Anything that goes against UK law will be unenforceable. For example, a ridiculously high interest rate will invalidate it or making loans to people who clearly can’t afford the rates or to repay them. Payday loans drew scrutiny on this latter issue and the FCA tightened up the rules to prevent further abuse. Just see how com ended up for an example of this.

Once your loan agreement meets these criteria, it can be legally binding. Legalo’s template helps you meet all these criteria.

Do you have to pay tax on a loan?

In the UK, loans themselves and the repayment of the capital element on them are not subject to income tax or capital gains tax, as HMRC does not consider them to be taxable income. If you borrow money, the borrower doesn’t need to pay tax on the loan amount or on the repayments. However, if the lender charges interest on the loan, then HMRC might consider it to be income and thus reportable to HMRC and chargeable to income tax.

How do you calculate interest on a loan?

When creating a loan agreement in which the borrower needs to pay interest, you will need to calculate exactly how much interest they will need to pay. Your contract needs to specify the interest rate, so that both parties can agree on it. By completing the following sum, you can work out how much interest the borrower will owe to the lender:

- Annual interest = Loan Amount x Annual Interest Rate

If the lender does not collect the interest annually, but instead periodically (e.g. monthly or quarterly), then divide the annual interest by the number of periods in a year, to work out the figure for each repayment period.

- Periodic Interest = Annual Interest / Number of Repayment Periods

To calculate the total interest, simply multiply the Periodic Interest by the total number of repayment periods.

- Total Interest = Periodic Interest x Total Number of Repayment Periods.