{kind=link}

{kind=link}

Debenture Agreement

Our debenture template:

- provision for fixed and floating charges

- Easy to edit, with full guidance notes

- UK lawyer drafted for reliability

How Does It Work?

-

1. Download

-

2. Edit

-

3. Print

-

4. Sign

Our debenture agreement template is for use when taking security over the assets of a company when making a loan to the company. The template is downloadable in Word format. Once purchased you can use it as many times as required.

Drafted by an experienced UK commercial solicitor and written in clear English, without the use of jargon, this agreement is simple to complete.

Use it to secure:

- a loan from an individual to a company; or

- a loan from a company to another company.

Don’t use it to secure a loan to an individual. Individuals cannot issue debentures – try a legal charge instead.

What does the Debenture Cover?

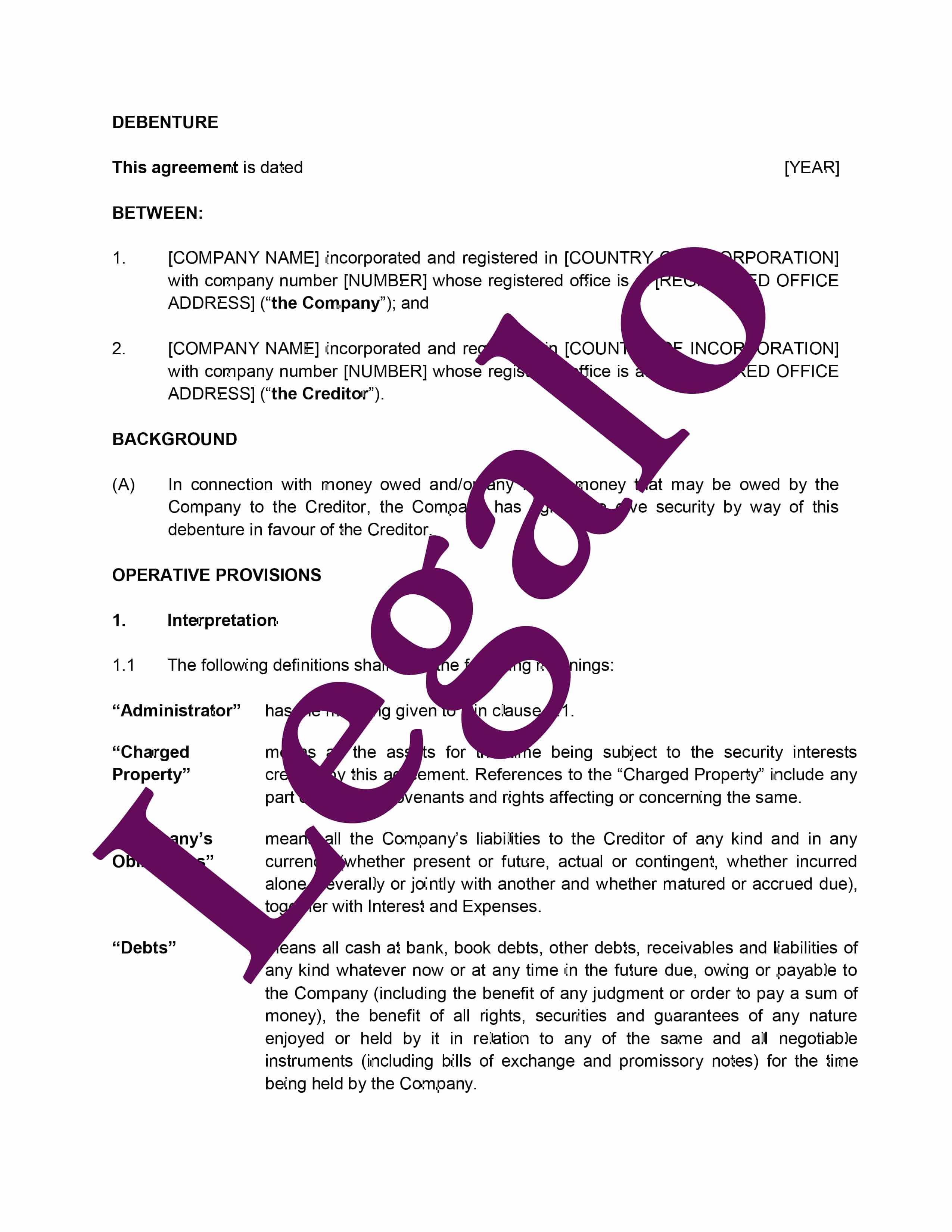

Our debenture template is for use where a creditor is to take a form of security over the assets of a debtor that is a limited company as security. Only companies can grant debentures – not individuals.

A detailed guide to completing the agreement is included but if you would like to read the detail of the actual clauses in the agreement then you can read our guide to the clauses in this debenture template.

Not sure if this is the right template agreement for you or not quite sure what a debenture is, then read on.

What is a Debenture Agreement?

If as a lender you think you might ever need security for your loan at any point, it is best taken at the point you make the loan. If it is taken later on, after the loan has been made, it may not be valid. This is particularly so if taken shortly before a borrower that is a company goes bust.

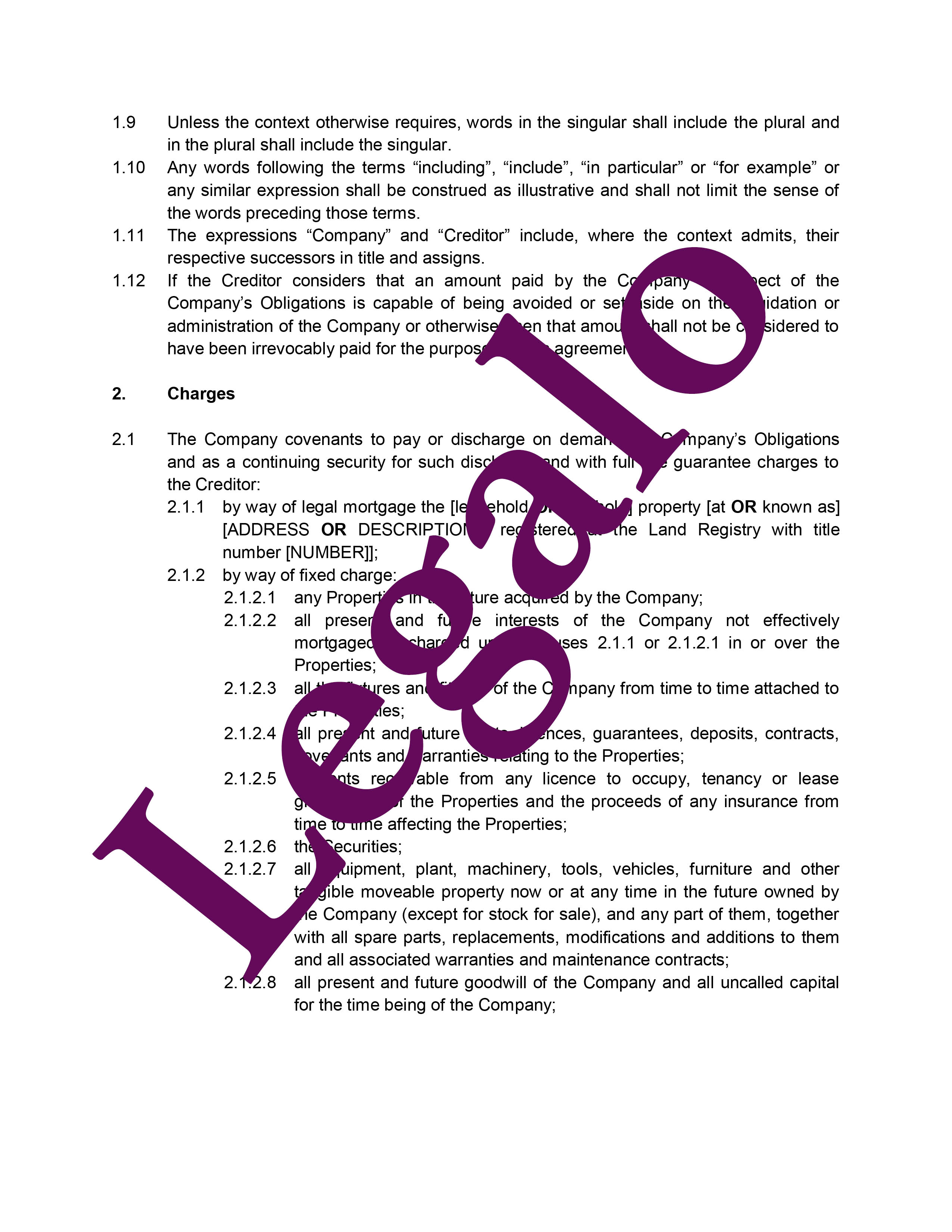

A debenture sets up a series of legal charges over all of the different classes of assets that a company might own. For example, if the company:

- has freehold or long leasehold property, the debenture imposes a mortgage (fixed legal charge) on them;

- acquires freehold or long leasehold property in the future, the debenture will impose a fixed charge on it;

- owns equipment, computers, vehicles and machinery, the debenture imposes a fixed charge on them;

- has money owed to it, e.g. by customers, the debenture imposes a floating charge on those book debts;

- holds cash in the bank, the debenture imposes a floating charge on it; or

- has stock, the debenture imposes a floating charge on it.

How does a Debenture work?

It works like a bank mortgage over a house or other land. Ultimately, it gives the creditor the power to sell the assets in question if the debtor has defaulted. Then it can recover the money owed to it. For example, default in the repayment of a loan owed to the creditor.

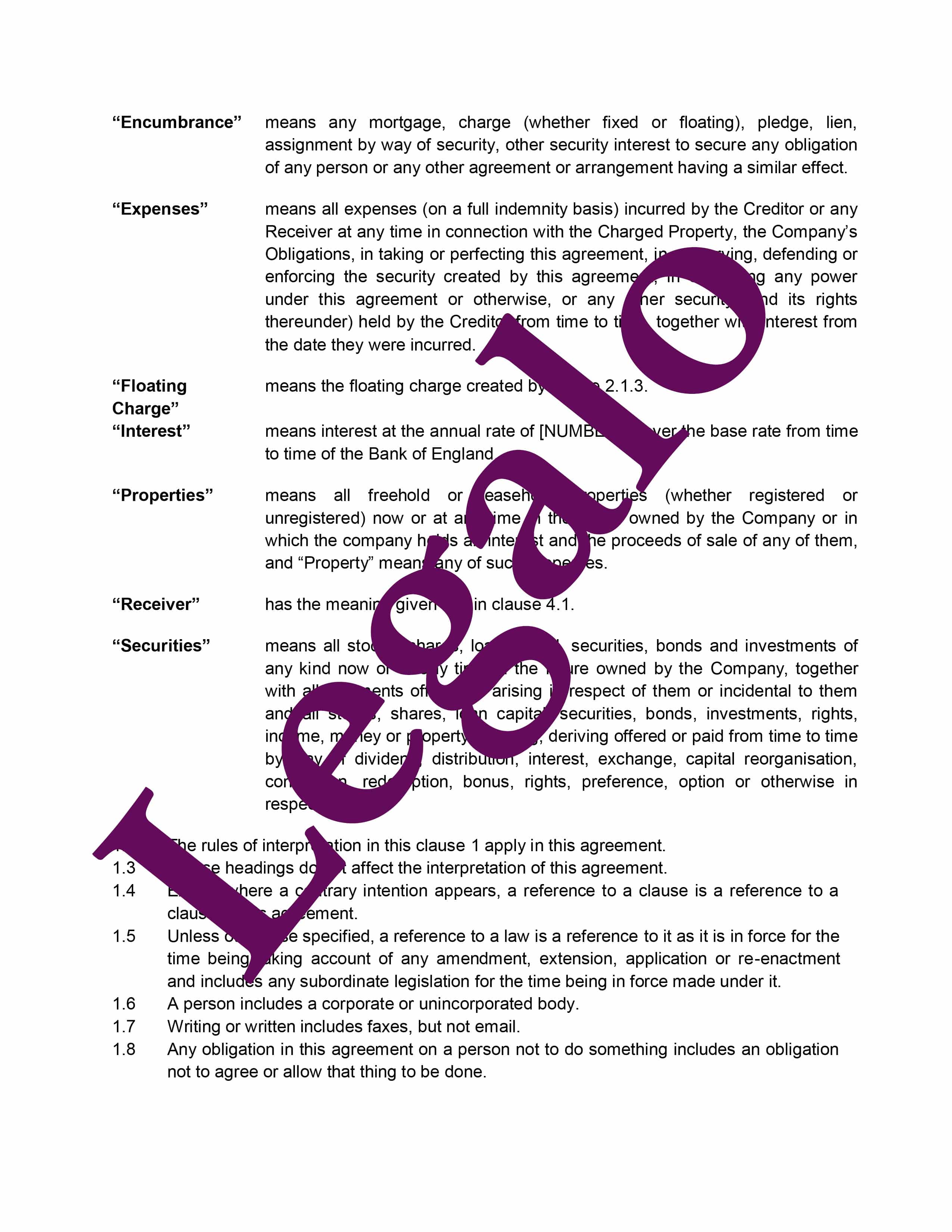

A “fixed charge” prevents the company from selling the assets in question. This tends to be over long-term assets that the company does not trade in, unlike stock. A floating charge permits the company to sell the asset (e.g. stock). However, when it acquires more stock to replace the stock it sold, the floating charge will extend to cover that new stock. If a critical event occurs in relation to the company, the floating charge can “crystallise”. This means it turns into a fixed charge, meaning the company can no longer trade in that type of asset. This would stop the company, for example, from selling the stock. Such an event might be the insolvency of the company, default in making repayments or another breach of its agreements with the creditor.

One minor difference between this debenture and the sort a bank takes over a company that banked with it, is that our debenture only has a floating charge on book debts and on cash at bank, instead of a fixed charge. This is because if you, as the creditor, are not a bank, then you cannot exercise the degree of control over the company’s cash and debts that a bank needs to for it to be entitled to a fixed charge in legal terms.

Loan Agreements, etc

You may be using this debenture in conjunction with one of our loan agreement templates, in which case, please use our “Secured Loan Agreement” template. Our debenture is designed to be used alongside a loan agreement, such as that one. If you need both then buy our Discount Pack, which has both of them in at a 20% discount. For an explanation on why you need both documents to work together, please see this blog article (references in it to a “legal charge” should be read as references to a “debenture” for your purposes): Do I Need A Loan Agreement With My Legal Charge?

You would only use our debenture to take security over a company. For individuals, you can take security by a legal charge over freehold property or long leasehold property they own.

Registration of the Security

Where you are taking security over a UK company, the security must be registered at Companies House. Use form “MR01”, which you can obtain here free of charge from Companies House. Strict deadlines and fees apply for this – full details are in the guide that accompanies the template.

If there is existing freehold or long-leasehold land that is registered at the Land Registry, then you also need to register the legal charge created by your debenture there. For more details on this and for the free form to use, please have a look at the Land Registry’s website. Again, fees will apply for the registration itself.

Release of security

If you need to have the debenture security formally released when the debt it secures has been fully repaid, then you can use our template Deed of Release of Security for this. You should also register the release by filing an “MR04” form at Companies House.

Guarantors

Also use this debenture to secure a guarantor’s obligations (most often regarding a loan or debt), if they have agreed to provide security. If relevant, then in this guide and the related template, treat references to the company as meaning the guarantor. Effectively it will be standing in the shoes of the original debtor to the extent of the guarantee. (If you need a template for a guaranteed loan, then Legalo has one available.)

NB In relation to companies standing as guarantor of a third party’s obligations, this is only lawful if there is a real commercial benefit to the company in its doing so. This is usually only in situations where:

- someone is paying the company to stand as guarantor of, say, a key shareholder’s obligations; or

- the company is acting as guarantor of the liabilities of another company in its group. For example, a parent company giving a guarantee in relation to its subsidiary.

If you are in such a situation, you should take independent legal advice from a company law specialist. The lawyer will understand this issue and can verify that it is being dealt with correctly. If you need help finding one, simply contact us.

FAQs

Below we have answered some of the most popular questions on debentures from the Internet.

What is a debenture?

As noted above, a debenture is a security that only a company or other corporate body can provide. It creates a series of charges over the company’s assets. The key to good security is to ensure the company has sufficient assets. Many don’t. The best security is still a first fixed charge on freehold property. Most companies do not own freehold property.

How do you set up a debenture?

Our template is the easiest and quickest way to get a debenture in place. To complete its set up, you need to register it. The first place to register it is at Companies House, which needs to be done in 21 days of its being signed. If there is any freehold property that the company owns, then the debenture also needs to be registered at the Land Registry. Then that’s it. If the company acquires any freehold property in the future, then, again, the debenture should be registered over it.

Who can create a debenture? Can an individual give a debenture?

As noted above, only a body corporate (generally a limited company) can issue a debenture. Individuals can grant legal charges over property they own, but cannot grant debentures.

What is an example of a debenture?

In the case of debenture bonds for loans, UK government bonds are an example.

Does a debenture have to be registered?

Yes. You must be register your debenture at Companies House within 21 days of its creation. This is a strict time limit. If the company has freehold property, then you must also register the debenture’s fixed charge at the Land Registry.

How risky is a debenture?

A debenture agreement is not risky if the company has good underlying assets that the lender can sell and turn into cash to repay the loan. Those assets might change over time and, if the company makes losses, they would reduce. This does make the debenture less safe in many cases. The lender should keep an eye on this.

If the debenture included a first fixed charge on freehold property, then even if the company makes losses, the lender still has the, hopefully, valuable property as security.

Who issues debenture certificate?

In the UK, we don’t have debenture certificates for this sort of security. This is a reference to a debenture bond. The borrower issues the debenture certificate in the case of a bond.

Do you register a debenture at Land Registry?

Yes, if the company owns land. The debenture creates a series of charges over the company’ assets, which include fixed charges on all freehold property it owns and fixed charges on any freehold property acquired in the future.

What are the different types of debenture?

A debenture agreement usually follows one type of format:

- creating a series of charges over the company’s property; and

- granting certain powers to the lender that it can use in the event of default in the repayment of the loan.

A debenture can also mean a bond issued by a company or a government in return for a loan. A lender can trade bonds for debts. They state the amount of interest due on the loan and when the borrower is to repay the loan. Investors see most government bonds as good assets, as most governments rarely default on their debts. Company bonds are not nearly as secure, and have ratings from the large rating agencies, such as Standard & Poor’s (S&P Global Ratings). Investors and rating agencies call the debenture bonds of companies with lower ratings junk bonds, and investors see them as pretty risky. A debenture bond is not like a debenture agreement. It does not create any security over the company’s assets unless it is a secured bond. An unsecured bond is more like an unsecured loan agreement.

What are the advantages of debentures?

Debenture agreements give the lender good control over the company’s assets, so long as it has sufficient assets to repay the loan in one way or another.

For the borrowing company, a debenture allows the company to utilise all of its assets (e.g. cash, land, stock, book debts owed to it) in order to maximise its borrowing power.

What is the disadvantage of a debenture?

For the lender, if the company has no freehold property, then the next best asset is often the debts that customers owe to the company (book debts). This is not as good security as a first fixed charge on freehold property, but there is usually a fair volume of such debts at any one time. Stock can also be a sizable asset in a trading company. However, it may take time for the lender or company to receive payment for such debts or sell such stock. If the company has little in the way of physical assets or book debts, then the debenture may not be terribly good security.

For the company borrowing and giving debenture security, this reduces the capacity of the company to borrow further. This is because it won’t have any free assets that it can use as security, as it will have given all of them as security under the debenture.

Is a debenture an asset or liability?

A debenture agreement is neither. The loan that the debenture secures is an asset (i.e. a debt the borrower owes) to the lender and a liability of the borrower. The debenture agreement is just the security for the debt.

A debenture bond is an asset for the lender and a liability of the borrower, as it represents the loan.

Guide to our template

We include a full detailed guide to this template, and to completing it, with the download. You can preview the guide here.